A Simplified Guide to Education Loans for Study Abroad

Table of Contents

- Understanding Why Education Loans for Study Abroad Matter

- Key Sources of Funding and Education Loans for Study Abroad

- Features and Requirements of Education Loans for Study Abroad

- Application Process for Education Loans for Study Abroad

- Factors Influencing Approval of Education Loans for Study Abroad

- Types of Education Loans for Study Abroad: Secured vs Unsecured

- Tax Benefits of Education Loans for Study Abroad

- Repayment and Moratorium Periods on Education Loans for Study Abroad

- Frequently Asked Questions About Education Loans for Study Abroad

Stepping into the world of international education is exhilarating, but the price tag can be daunting. When the dream seems out of reach, education loans for study abroad become the key that opens new doors. We have witnessed countless students overcome financial barriers, and there’s one thing that stands out—expert guidance truly makes a difference. We at Galvanize Global Education continue to lead millions of students to top global universities, not just with admissions counseling but also with education loan assistance.

Understanding Why Education Loans for Study Abroad Matter

Every year, nearly 70,000 Indian students secure education loans to study abroad. With tuition fees, living costs, and travel expenses piling up, an education loan becomes much more than just a financial resource – it’s a strategic investment in a future rich with opportunities. Galvanize Global Education’s approach to admissions counseling includes comprehensive support for education financing, ensuring that students put their best foot forward at every stage.

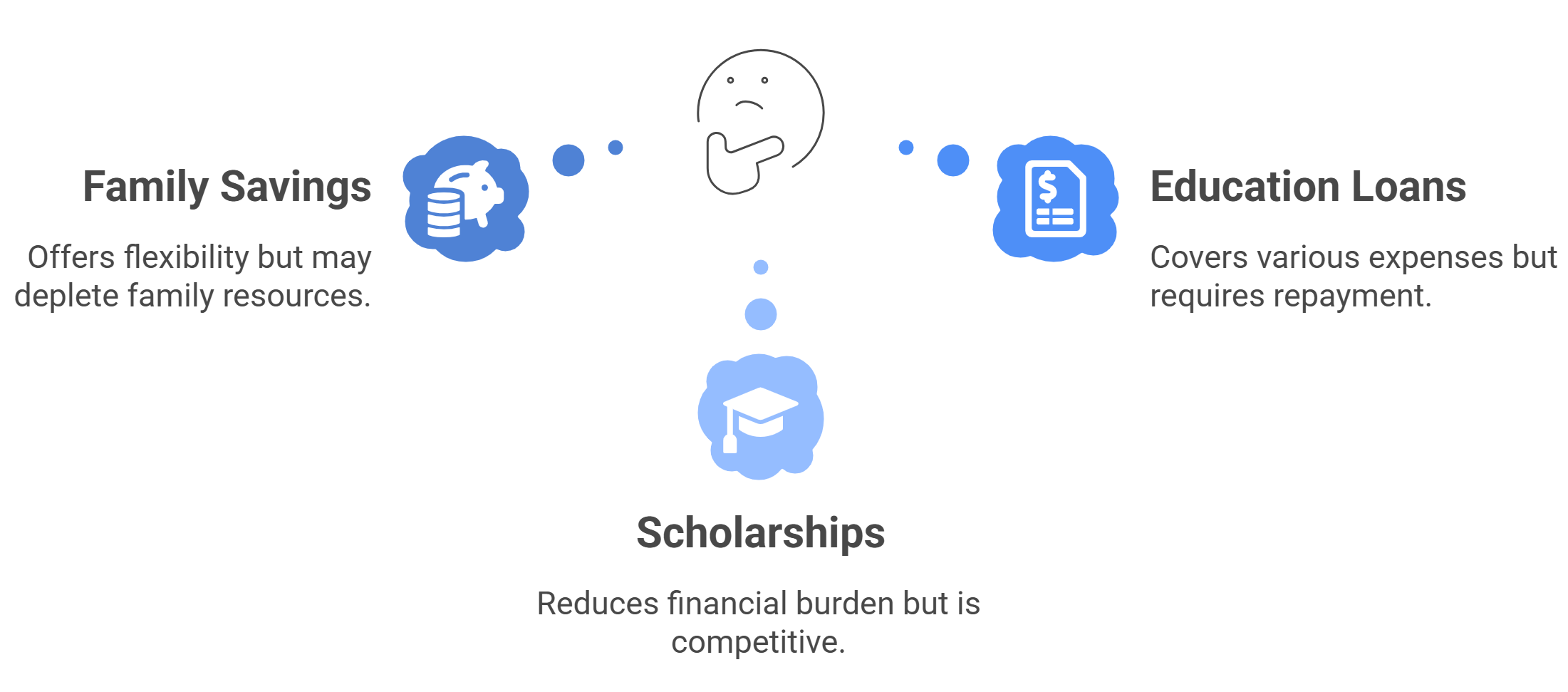

Key Sources of Funding and Education Loans for Study Abroad

Students often tap into a mix of resources: family savings, scholarships, and, increasingly, education loans for study abroad. Loans offer flexibility that other options might not, with most covering tuition, living costs, exam fees, travel, and even pre-admission expenses. Innovative fintech lenders now join leading banks and NBFCs; therefore, comparing all options is essential for making informed decisions. This is where Galvanize Global Education’s data-backed counseling becomes your secret weapon. By providing loan comparisons based on your profile and needs.

Features and Requirements of Education Loans for Study Abroad

The typical borrower is between 18 and 35 years old, applying for undergraduate, postgraduate, or doctoral programs. Both secured (collateral-backed) and unsecured loans are available; secured loans provide higher amounts and lower interest rates, while unsecured loans offer speed and accessibility but often come at a higher cost.

Loan application packages must include admission letters, identity and address proof, academic transcripts, income statements, asset details for you and any co-borrower (usually a parent), and bank statements. Galvanize Global Education walks you through every step, anticipating documentation pitfalls before they occur.

Application Process for Education Loans for Study Abroad

Applying for an education loan starts with selecting the right bank or lender. Submit your application online or offline with all required documentation. The lender reviews the paperwork, evaluates creditworthiness, and, for secured loans, assesses the collateral value. Once approved, funds are disbursed according to your university calendar, usually covering fees and living costs in tranches. Galvanize Global Education’s process includes university shortlisting and financial planning, easing these transitions.

Factors Influencing Approval of Education Loans for Study Abroad

Banks examine a borrower’s academic record, future employability, credit score, the reputation of the chosen university, and collateral or guarantor status. A strong profile comprising academic excellence, recognized university admission, and robust financials boosts approval chances. Galvanize Global Education’s expert counselors specialize in profile enhancement, helping students present their application in the best light.

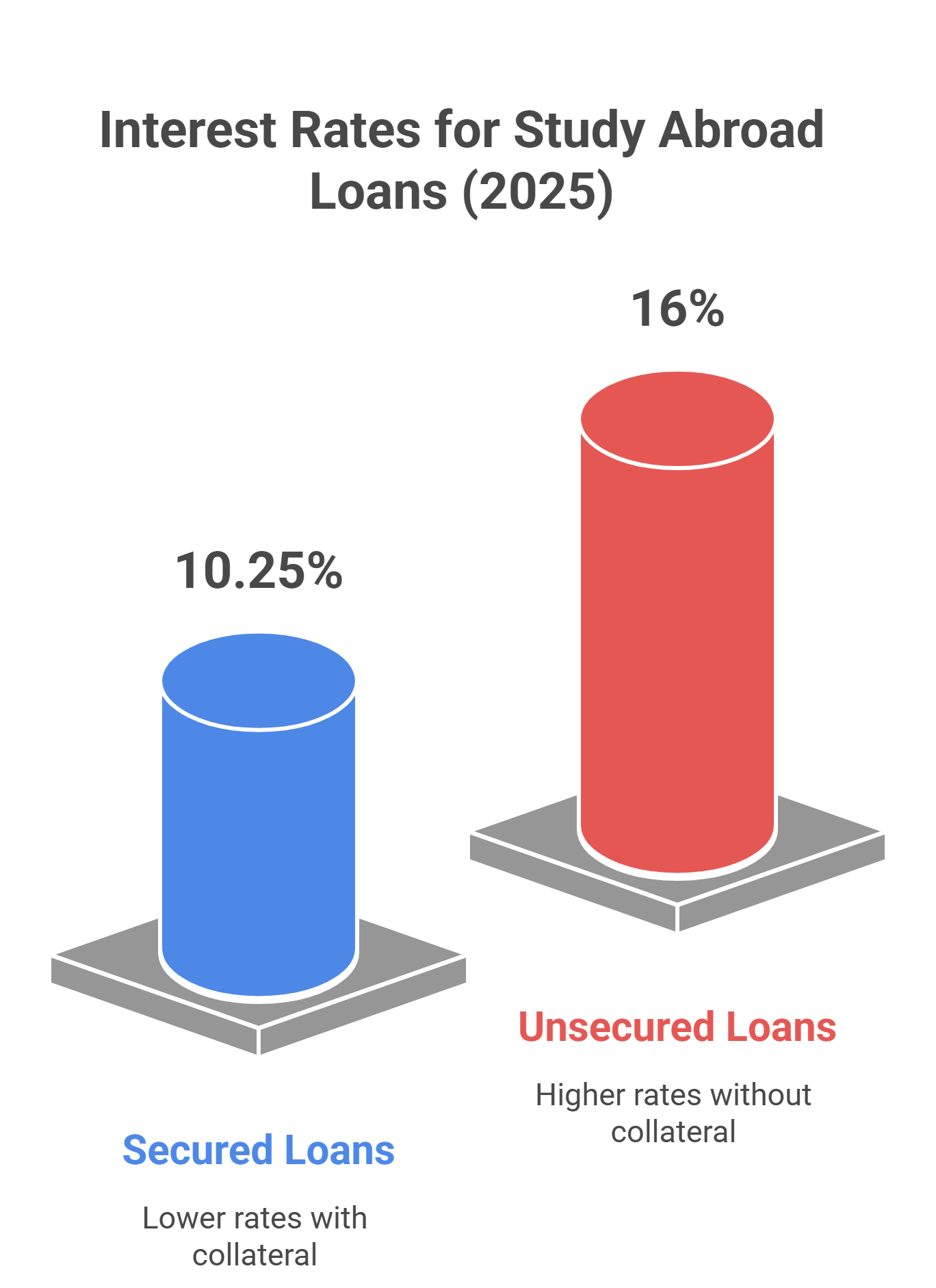

Types of Education Loans for Study Abroad: Secured vs Unsecured

Secured vs Unsecured

Secured loans require tangible assets (like property or fixed deposits) as collateral, offering lower interest rates, from about 9% to 11.5% for 2025. Unsecured loans, often provided by NBFCs and fintech lenders, can reach up to 16%, depending on creditworthiness and lender policies. While unsecured loans may seem attractive for speed, always weigh the pros and cons carefully.

Tax Benefits of Education Loans for Study Abroad

The Indian government offers a tax break under Section 80E, allowing individuals to claim a deduction on the entire interest paid for eight years from the start of repayment, with no upper limit. Only the interest portion is deductible, not the principal, and only if the loan is from recognized banks or NBFCs. Parents can also claim this benefit if they are the loan applicants for their child’s higher studies.

Repayment and Moratorium Periods on Education Loans for Study Abroad

Education loans typically have a repayment window of 5 to 15 years. Most providers allow a moratorium period, covering the study duration and up to one year for job search, during which full repayment isn’t required. Government banks permit interest-only payments or even deferred payments during this grace period. The EMI (equated monthly installment) amount varies depending on the tenure and whether the loan is secured or unsecured.

Repayment starts once the moratorium ends, with initial EMIs mainly covering interest before transitioning to principal payments. Choosing the right loan and planning for timely repayment are essential. Galvanize Global Education continues to assist students well past admission day, helping navigate loan repayment strategies and financial planning for their study abroad journey.

Frequently Asked Questions About Education Loans for Study Abroad

Students often ask about the best banks for loans, processing times (usually up to 45 days for secured loans), eligibility for tax benefits, and the role of academic records in approval. For all these queries, Galvanize Global Education is your one-stop solution, combining admissions expertise with hands-on education loan assistance.

Start your journey to a global education with confidence, knowing that education loans for study abroad, when chosen with expert help, can be the stepping stone toward realizing dreams.